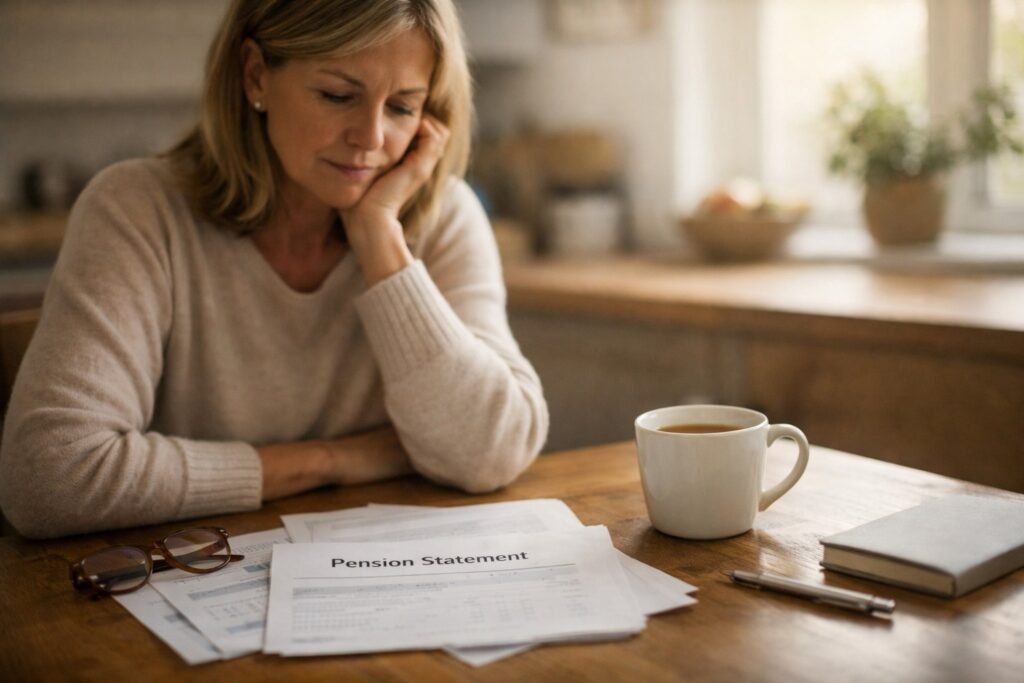

When’s the last time you pulled up your pension statements and took a good, hard look at them or told yourself you’d deal with them later?

If you’re like most people I work with, those statements are gathering dust in a drawer somewhere or buried in an email folder, still in their envelopes and unopened.

You probably walked past that drawer this morning. Maybe you even opened it to get something else. You saw the envelope with the company logo and immediately closed the drawer.

That’s not because you’re careless. On the surface, things seem broadly under control.

So when someone asks how retirement planning is going, you say what most sensible people would: “Getting there”, “On track, mostly”, or “We should be fine.”

And for a long time, that was enough.

But financial planning after 50 is different.

At this stage, roughly fine doesn’t really cut it anymore.

What once felt like flexibility now feels like a background worry you can’t quite switch off.

The Approach That Worked… Until it didn’t

Being vague about money isn’t a flaw. It’s a way to cope. If you don’t lock things in, you don’t have to face hard truths. You don’t have to commit too soon or shut doors you might want later.

For high earners, especially, this worked for a long time. In your 30s and 40s, time was on your side. Markets bounced back. Income usually grew. Mistakes could be undone. Staying vague felt smart. Even responsible. After 50, though, something changes. Time doesn’t stretch the way it used to. And the habit that once protected you quietly starts holding you back.

What “we’re probably fine” Usually Means

Usually, what they really mean is: I haven’t looked closely enough to be sure.

If I asked you, without guessing, could you tell me:

- What will you have available in your first year of retirement?

- Whether your current spending looks anything like what you’ll need then?

- Who earns what, when, and where the gaps are?

Most people can’t.

Not because they can’t do it, they’ve just been vague for so long that being exact doesn’t feel necessary anymore. Until it suddenly becomes very necessary.

Research from Which? shows that one of the biggest obstacles to effective retirement planning after 50 isn’t a lack of money; it’s not knowing the real numbers. Estimates replace facts, and uncertainty fills the gap.

How Vagueness Starts Leaking into Real Life

The real cost of financial fog isn’t just the fear of running out of money.

It’s hesitation.

You’ve been offered the role with less travel, better hours, and more breathing room. Maybe more than once. Each time you’ve said you need to think about it.

What that usually means is you’ve done the exact mental maths you always do, rough figures, moving targets, nothing grounded. And because it still feels unclear, you’ve said no.

Again.

Helping your adult children? You want to, but you don’t know what it does to your timeline.

Cutting back your hours? Possibly, but are you two years from retirement or seven?

When you don’t have clarity, every decision feels like it might be the wrong one. So you stay cautious. Keep working. Keep postponing the life you want.

The issue usually isn’t a lack of resources. It’s not knowing where you really stand.

I recently worked with a client who delayed helping her daughter with a house deposit for over a year. Not because she didn’t want to help, but because opening the numbers felt too exposing. She kept saying, “Let me look at them properly.” She never did.

Why Looking Properly Feels Uncomfortable

If clarity is so helpful, why do so many capable people avoid it?

Because clarity asks something of you.

You’re not waiting for the right moment; you’re waiting until you feel brave enough to.

Looking properly means facing what’s there, not what you hope is there.

Maybe you’ve been spending more than you realised, the gap is bigger than you expected, or retirement isn’t as close as you’ve been telling yourself.

Vagueness softens the blow.

Clarity asks you to deal with reality.

So it’s easier to stay in the fog for a bit longer.

After 50, that “bit longer” goes quickly.

What Happens When You Get Specific

Someone finally sits down and looks properly, not estimates, not best guesses, but real numbers.

And almost always, one of two things happens.

Either they realise they’re in better shape than they thought and feel immediate relief.

Or they discover there’s a gap, but now it’s clear, measurable, and fixable.

Both are far better than living with constant uncertainty.

Once you know, the mental weight lifts.

Decisions stop feeling so loaded. Saying yes feels grounded, and saying no stops feeling guilty.

Retirement becomes something you move towards deliberately, rather than something you edge around.

Clarity doesn’t reduce your choices.

It makes them real.

The people who feel calm in their 60s aren’t always the wealthiest. They’re usually the ones who became clear in their 50s and made conscious decisions from there.

Research from Age UK shows that uncertainty about finances is one of the biggest sources of anxiety for people approaching retirement, often because they’ve never sat down with the full picture.

What Financial Clarity Before Retirement Really Looks Like

This isn’t about perfection; it’s about sleeping well at night.

When financial clarity is in place, something subtle but significant shifts:

- You stop framing your future in defensive terms

You’re no longer thinking in terms of “making sure nothing goes wrong.” The question becomes: what do you want the next phase to be?

- Your sense of timing changes

You’re not counting down vaguely or telling yourself you’ll reassess “soon.” You have a clearer sense of sequence, what happens first, what can wait, and what no longer matters.

- Your self-image updates

You stop seeing yourself as “not quite ready yet” and start relating to retirement as something you’re actively shaping rather than bracing for.

- You separate risk from discomfort

Not everything that feels uncomfortable gets labelled as dangerous. You can distinguish between real financial risk and emotional unease.

- You relate to money as a support, not a threat

Money stops feeling like something that could trip you up at any moment. It becomes a tool you understand well enough to trust.

It doesn’t make life predictable, but it steadies your direction.

Why vagueness gets risky after 50

Being vague helped you for years. It gave you flexibility.

But in retirement planning after 50, it starts doing the opposite.

Time hasn’t run out, but room for imprecision has.

Every year you remain unclear costs you, not just financially but also in delayed decisions and missed opportunities.

Moving from vague to clear doesn’t have to be dramatic. It can be done one afternoon, an honest look or one proper conversation.

What most people feel afterwards isn’t panic.

It’s a relief.

The Bottom Line

If this sounds familiar, you’re not alone. Most people stay vague longer than they need to, most especially high earners. Clarity can feel exposing, but over time, vagueness costs more than honesty.

If you’re ready to stop guessing and know where you stand, that’s the work we do at RetireFulfilled.

The pension statements will still be there tomorrow.

But tomorrow, you’ll be one day closer to retirement and one day further from being able to change what’s inside them.

When you’re ready, let’s talk.