Emma 54, is a marketing director in London, earns £120,000, drives a BMW, owns a stylish Clapham flat and goes on three holidays a year. By every measure, she is on course in wealth building. She also has £1,897 in savings. Despite a decade of “financial responsibility,” she’d been living a £120k lifestyle on £68k take-home per annum, the difference being financed by credit and delusion. She’s not reckless. She’s stuck in spending traps sabotaging wealth accumulation, a problem that most high earners don’t even see.

After 30 years as a chartered accountant, in which I’ve observed professionals trip over the same spending traps that undermine wealth building, Emma is typical and not an exception.

Out of the professionals investigated, 73 per cent of those earning more than £75,000 have fewer than three months’ worth of expenses saved. Even more shocking? Those earning £150,000+ were more likely to be living paycheque-to-paycheque than those earning £45,000.

By 2030, 60% of those making six figures will actually be less well off than the median income earner of today, even though their salary would triple.

The Neuroscience Behind Salary Addiction

Every rise in pay hits the dopamine pathways in your brain, akin to being rewarded with a good prize. UCLA research has demonstrated that a wage increase affects the reward centre of the brain in much the same way as addictive substances. You get high for a few weeks and then your brain adjusts; you have to have another financial hit.

Your brain is not your friend when it comes to building wealth.

The addiction cycle:

- New money comes in: Job, promotion, bonus payouts.

- You feel phenomenal: Get all high on success.

- The real story: New money feels normal in just a few weeks

- Crash occurs: thrill dies; increased costs remain

- You need a fix: Chase the next raise while wealth stagnates

The 5 Spending Traps Sabotaging Wealth That Keep High Earners Broke

These traps silently siphon off wealth from high earners, regardless of their earnings.

Spending Trap #1: The Gross Income Mirage

HR likes gross salaries because they make you sound 40% more wealthy than you actually are.

That £80,000 salary? So you really have £52,000 to build wealth. But your brain plans around the phantom £28,000 that never arrives.

Having managed multi-million pound budgets, I see how pay structures can inflate perceived value and restrict true financial independence.

And that’s the first illusion.

Spending Trap #2: The Employer Match Con Job

The auto-enrolment seems robust, with 5 percent from you and 3 percent from them. But psychological manipulation is the thing that slows wealth growth.

Most UK employers match up to 10-12 percent if you do too, but few will tell you that.

My client David lost £4,200 a year for seven years. That’s £89,000 wiped off the value of free money.

For over a decade in my finance career, I have observed how unclaimed pension matches are quietly slicing employer costs and cutting into employees’ paychecks.

Money left on the table is free money, wealth lost forever.

Spending Trap #3: The Death Spiral of Lifestyle Inflation

The most expensive lie preventing financial freedom: “You deserve to enjoy your success.”

According to my research, for every £10,000 earned in additional pay rises, just £400 will go towards wealth, the other £9,600 leaks out in lifestyle upgrades.

Marcus more than doubled his salary from £45,000 to £75,000. His expenditure tripled, from £35,000 to £69,000. He was making more, but never felt further from freedom. This is not how the system is supposed to work.

Lifestyle upgrades are rewarding, but they’re silently erasing your progress. See our guide on The Poverty Mindset in Retirement

Spending Trap #4: Luxury Benefits That Appear to Be Rich But Aren’t

Fancy benefits are an imitation of wealth building, but they don’t actually grow your finances.

That £5,000 car allowance? After tax, it’s worth £2,500. If you took the cash option, you’d have £3,500 to invest.

Stock options? They’re either winning or losing lottery tickets, given that their success is dependent on company performance, vesting, and market timing. Not a solid wealth foundation.

Benefits seem impressive, but rarely amount to genuine financial growth.

Spending Trap #5: The Comfort Zone (Literally Costs You Millions)

Job security sounds secure but often pays less than market, stalling wealth accumulation.

The “loyalty penalty” is costing UK workers £8,000 a year. Over the course of a career, comfort can come for £300,000, money that would buy someone independence.

Internal raises average 3-5%. Strategic job moves? 15-25% jumps that can rapidly accelerate wealth.

Comfort is the safe choice, and it’s the most expensive trap there is.

Avoiding these traps is not only smart but also essential for the long-term transformation of income into wealth.

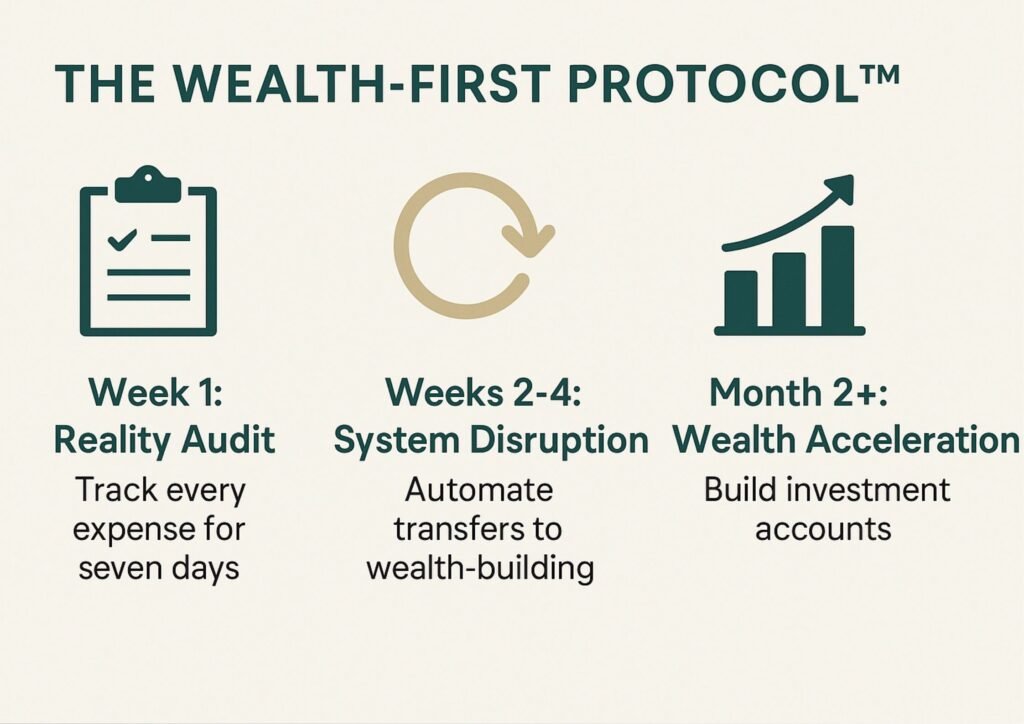

Breaking Free: The WEALTH-FIRST Protocol

After thirty years of watching professionals sabotage their financial future with big salaries, I built a system to break salary addiction and spending traps, for good.

Week 1: Reality Audit – Record every single expense for seven days. Identify spending triggers that block wealth growth. For most clients, 40% of their money disappears into a set of unnamed categories. Compute missed employer pension contributions and free up additional funds to grow your savings.

Weeks 2–4: System Disruption – “Automation before temptation” — automate direct payments to wealth-building activities before your brain gets in the way.

Use the 50/25/25 Wealth Rule:

- 50% of the raises to investments

- 25% to debt or emergency fund

- 25% to lifestyle upgrades

Month 2+: Wealth Acceleration – Build assets that grow even if you lost your job or woke up in a bad mood. Monitor net worth monthly by numbers, not by feelings. Research your market value yearly. Negotiate if you’re underpaid by 15% or more, or leave to maximize your earning potential.

Client Testimonial: Jennifer’s Wealth-First Breakthrough

I used to think that earning £95k meant I was doing ok. But I had no real plan; I was just spending and saving at random, crossing my fingers and hoping for the best.

“Once I implemented the WEALTH-FIRST Protocol, everything flipped. I created £67,000 of investable assets in less than two years. It’s not just that I saved, I learned to grow wealth intentionally.”

“Now I have systems that operate without my involvement. My money flows automatically, my investments grow steadily, and I leverage my long-term targets, not short-term forces. I’m finally creating the type of financial future that I used to want for myself.”

Your Choice: Wealth or Illusion

The system is designed to maximise your income and minimise your wealth. It doesn’t reward responsibility, it rewards spending.

But these spending traps sabotaging wealth can be easily avoided.

The WEALTH-FIRST Protocol exists to break those chains, restore control, and fast-track your path to financial independence.

It’s not whether you can afford to change; the question is: Can you afford not to?

But eliminating spending traps sabotaging wealth, is just the start.

Final Warning: Retirement Is Not Automatic

Most professionals who escape these financial pitfalls assume traditional retirement planning will handle the rest.

It won’t.

The same system that created these spending traps has retirement myths that could destroy everything you’ve worked for. Don’t stop at earning more, build structures that protect what you’ve earned.

At this stage of life, your time is more valuable than your salary. Don’t let avoidable money traps steal years you can never get back.

“What’s it going to be: one more year of lifestyle inflation that keeps you dependent on a salary, or financial freedom that will allow for genuine financial independence and retirement options.

Next step: Start with our free RetireFulfilled Life Audit to assess your true financial position.